Introduction – Born with Nothing but Fire in his belly

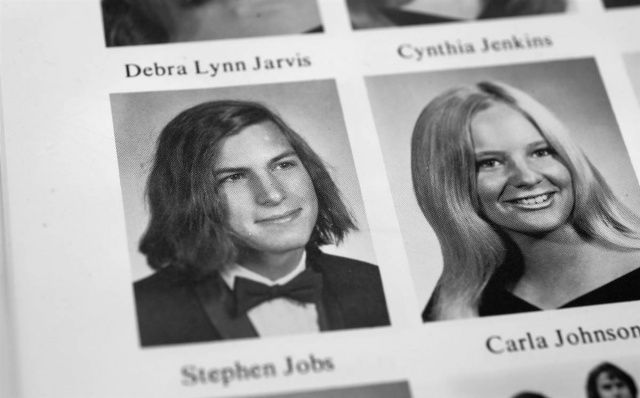

It all began in 1956 in the heart of horse country, Lexington, Kentucky. Picture a small home, chipped paint, a cracked driveway, and a fridge that was more often empty than full. This was the world John Bryan Morgan was born into. His childhood wasn’t bathed in luxury. No designer clothes, no trust funds, no summer getaways to Europe. What he had instead was a relentless fire in his belly, a hunger for something bigger.

Illustration1: John Morgan, the legend behind it all.

John was one of five siblings in a working-class family that often struggled to make ends meet. His father, a meat cutter with a troubled relationship with alcohol, would sometimes disappear into his vices, leaving his wife, John’s mother, to keep the family afloat. She was the real-life Wonder Woman. No cape. No superpowers. Just grit and an unbreakable sense of duty.

Even as a child, John knew life wasn’t fair. Other kids had allowances. He had chores. While others played video games, he was mowing lawns, washing dishes and hustling in every way he could.

And yet, even amid poverty, there was something special about young John. He was observant, sharp and most importantly, he had a dream. He wasn’t sure what it was yet, but he knew it didn’t involve staying poor.

Illustration 2: Kentucky, the humble start of John Morgan

College Dreams and Detours

John was determined to break the cycle. He knew education was the key, the great equalizer. He managed to claw his way into the University of Florida, a major leap for a kid from the working-class South. But college wasn’t a picnic. It was a battlefield.

To afford tuition, John worked a series of odd jobs, from dishwashing to nighttime security. He studied by the dim glow of streetlamps. He skipped meals. He bought used textbooks with notes scribbled all over them. But he never complained. Not once. Because he was building his future, one late-night cram session at a time.

After undergrad, John set his sights on law school. He got into the University of Florida Levin College of Law, where he was surrounded by peers from elite families, meaning kids who rolled up in BMWs while he was still patching holes in his shoes. But he didn’t care. He wasn’t there to impress, he was there to dominate.

He graduated in 1983, not just with a degree, but with a vision. He didn’t want to work for the rich. He wanted to fight for the people who had no voice, people like his mom, like his friends back in Kentucky, like himself.

Illustration 3: Morgan didn’t let the fact that he wasn’t rich or his social status bring him down.

The Birth of a Giant: Morgan & Morgan

In 1988, John Morgan did something insane, he left the comfort of an established firm and started his own with barely a handful of clients and next to no money.

He and his wife Ultima, a fellow lawyer, worked from a tiny office in Orlando, scraping together clients and praying they could make rent. There was no glitz, no glam, no waiting list of millionaire clients. It was just John, Ultima, a desk, a phone and a dream. But John had something most lawyers didn’t, the courage to advertise.

Back then, legal advertising was frowned upon. It was seen as “low-brow” even tacky. But John saw the future. He started running commercials, putting up billboards and buying ad spots on radio and TV. It was revolutionary. His face became instantly recognizable. His firm’s phone began to ring off the hook. And slowly but surely, Morgan & Morgan became a name people trusted.

Traditional firms sneered. Some even mocked him openly. But guess what? It worked. The phone lines lit up. Working-class Americans, immigrants, single mothers, veterans and everyday folks finally saw a lawyer who seemed to get them, a lawyer who didn’t look down on them, but stood beside them.

John knew that justice shouldn’t be reserved for the rich. He created a firm that operated on contingency meaning clients paid nothing unless the firm won. This flipped the power dynamic of law on its head. Suddenly, people who could never afford an attorney were getting high-powered representation. And they were winning.

Illustration 4: John Morgan’s formula of success lies in his use of advertisement.

Word spread. Morgan & Morgan began adding attorneys. Then offices. Then entire teams dedicated to intake, investigations, case management and trial. The small Orlando firm morphed into a regional force, then a national powerhouse.

But the firm wasn’t just growing, it was innovating. John implemented cutting-edge call centers and custom legal software to manage thousands of cases simultaneously. He invested in digital ads and SEO when other firms were barely online. He brought in experts in analytics, data and marketing to scale the business like a Silicon Valley startup.

By the 2000s, Morgan & Morgan had become a juggernaut. John kept his foot on the gas, opening offices in nearly every major city. The firm handled cases involving everything from medical malpractice and product liability to class actions and even civil rights.

Today, Morgan & Morgan has over 800 attorneys and 3,000 staff members. It serves clients in all 50 states and handles more than half a million cases each year. It’s not just the largest injury law firm in America, it’s one of the most recognized legal brands in the world.

Illustration 5: Morgan & Morgan has now more than 800 attorneys and run ads nationwide not only in Orlando where it all started.

John Morgan didn’t just start a law firm. He built a legal empire with a mission so clear it’s tattooed on the American psyche: “For The People.”

And that empire? It all started in a tiny Orlando office, with a man who believed that no one should have to fight alone.

From the Courtroom to the Boardroom

John Morgan didn’t just want to win cases, he wanted to bend the entire legal universe to his will.

Picture this: most lawyers were grinding away on measly slip-and-fall cases, chasing billable hours like hamsters on a wheel. John? He was building an empire. While the rest of the legal world was stuck in the 1980s, he was already thinking like Jeff Bezos with a briefcase.

He turned his firm into a litigation factory, but not in a sleazy ambulance-chaser way this was industrial-strength lawyering. Car accidents? Handled. Medical malpractice? Crushed. Class-action lawsuits? Bring it on. If David had a case against Goliath, Morgan & Morgan would’ve filed it before sunrise.

He pioneered a flat-fee structure, built a literal in-house call center to handle thousands of daily inquiries, and invested in tech like he was the Mark Zuckerberg of lawsuits. Imagine Apple HQ, but instead of iPhones, they were cranking out million-dollar verdicts.

Soon, he was on the talk-show circuit, dishing out unfiltered wisdom. He wrote books that didn’t just sit on dusty law school shelves, they hit bestseller lists.

His book “You Can’t Teach Hungry” was part pep talk, part street-fight manual, and part “Morgan gospel.” The thesis was simple: hustle like hell, be unapologetically yourself and never forget who you’re fighting for.

The Man behind the money

Now, you’d think a billionaire lawyer would be a stiff in a tailored Armani suit, sipping a $500 Scotch in some mahogany-lined office. Not John.

Illustration 6: Morgan was never stiff or elitist like other lawter, but he was relatable and liked the same things as an average american like a good Cuban sandwitch.

The man loves fried chicken. He loves Cuban sandwiches so much he’s practically a sandwich influencer. He puffs cigars like he’s starring in his own gangster flick, and he tweets jokes that make you wonder if your lawyer is secretly running a comedy club on the side.

He’s approachable, funny, and dare I say it dangerously relatable. And that’s why people adore him.

But peel back the jokes, and you find someone who cares deeply. Morgan has donated millions to causes like education, poverty relief, and criminal justice reform. One of his fiercest crusades? Medical marijuana.

This wasn’t about trend-chasing or headlines. This was personal. His brother, Tim, suffered from a devastating spinal cord injury, and medical marijuana was the only thing that gave him relief. John didn’t just sympathize, he fought. He poured millions into Florida’s 2016 Amendment 2 campaign and helped legalize medical marijuana statewide.

Not because it was fashionable. Not because it was profitable. But because it was right. Because family came first

The Billionaire Nobody Saw Coming

John Morgan didn’t wake up one day and say, “I want to be a billionaire.” He just kept building, winning, investing and suddenly, there it was.

Hotels? He bought them. Real estate? He stacked it like Monopoly pieces. Cannabis startups? Yep, he planted those seeds too. By the time anyone noticed, John had quietly become the billionaire nobody expected.

Sure, he’s got the toys: a mansion in Lake Mary, Florida, that looks like something out of MTV Cribs.

A fleet of cars. A private jet. A yacht. Probably a secret lair under the mansion for good measure.

But here’s the kicker: he’s still the same fried-chicken-loving, Cuban-sandwich-tweeting, people’s lawyer he always was. If you ask him about his proudest achievement, he won’t say “the billions.” He’ll say it’s his employees who love him, the thousands of clients whose lives he helped rebuild, and the fact that when people hear the name “Morgan,” they think trust.

Illustration 7: Morgan didn’t let his money change who he was.

The Media Mogul and the Meme Machine

Advertising? John Morgan doesn’t just do it, he dominates it. His law firm commercials are the stuff of legend. Funny, bold, slightly absurd and absolutely unforgettable.

And then there’s social media. Most billionaires hire a PR team to write robotic posts. John Morgan? He’s tweeting his own jokes, ranting about insurance companies, and casually dropping lines about running for president. One day he’s a lawyer. The next? A meme.

But here’s the genius: he leaned into it. He became the meme. He is the meme. He understood what most tycoons don’t: in the modern world, authenticity beats polish. Every time.

Illustration 8: John Morgan used memes, tweets and advertising heavly to his advantage.

For the People

Everything John Morgan built, everything, comes back to one mantra: For The People.

It’s not just a slogan slapped on a billboard. It’s the heartbeat of his firm. Today, Morgan & Morgan handles over 500,000 cases a year, a mind-boggling number that makes them less of a law firm and more of a justice delivery system.

He mentors young lawyers, invests in progressive causes and keeps pushing the boundaries of what a law firm can do. His sons are stepping into the game, learning the ropes, gearing up to take the Morgan legacy even further.

And John? He’s not even close to done. He might run for office. He might launch a bourbon brand called “For the Pour.” He might buy a baseball team just for the fun of it. Whatever it is, you can bet it’ll be big, bold, hilarious and very, very John Morgan.

Final Thoughts: The Legend of John Morgan

From the dirt roads of Kentucky to billion-dollar boardrooms, John Morgan’s story is the ultimate “American dream with a punchline.”

He didn’t just beat the odds, he rewrote them. He showed us that grit, guts and a sense of humor can take you from nothing to an empire.

He started with nothing. He gave everything. And he built a kingdom, for the people.

And if you don’t believe me, just wait because the next chapter of John Morgan’s story is probably going to be wilder than the last.

Illustration 9: John Morgan knew the power of humor and advertising.

India is more than just a country, it is a civilization that spans thousands of years, a vibrant continent in its own right, and an economic marvel constantly in motion. With a history that stretches back over five millennia, India remains one of the world’s oldest cultures while simultaneously being one of the youngest and fastest-growing economies on the planet.

Today, it stands as the most populous nation on Earth, the fifth-largest economy by nominal GDP, and a powerhouse of innovation and entrepreneurship. The economy of India is a developing mixed economy with a notable public sector in strategic sectors.

Known as the world’s largest democracy, India is a federal republic composed of 28 states and 8 union territories. It is a nuclear-armed nation, a member of influential groups such as the G20, BRICS, and the World Trade Organization, and holds a pivotal position in the Indo-Pacific region both strategically and economically.

As of 2024, India’s nominal GDP reached nearly $3.9 trillion, edging past the United Kingdom and approaching the size of Germany’s economy. When measured in purchasing power parity terms, India ranks third globally behind China and the United States. This remarkable economic ascent is fueled by a young and expanding population of 1.44 billion people, a rapidly growing middle class, and a labor force increasingly skilled in technology and services.

his article explores the complex and fascinating story of India’s economic evolution, from its early days of immense wealth through the hardships of colonialism, the challenges of socialist policies, and finally the remarkable liberalization that catapulted the nation into the global spotlight. Whether you are an investor, student, or simply curious about global affairs, India’s economic journey offers profound lessons in resilience, ambition, and transformation.

Historical Background

India’s history as an economic power dates back thousands of years, when it accounted for roughly a quarter to a third of the world’s GDP. During ancient times, great empires such as the Mauryas, Guptas, Cholas, and later the Mughals presided over prosperous kingdoms that exported textiles, spices, gems, and rich cultural knowledge to distant lands. India’s early economy was sophisticated and globally connected, making it one of the wealthiest regions on Earth.

India’s history as an economic power dates back thousands of years, when it accounted for roughly a quarter to a third of the world’s GDP. During ancient times, great empires such as the Mauryas, Guptas, Cholas, and later the Mughals presided over prosperous kingdoms that exported textiles, spices, gems, and rich cultural knowledge to distant lands. India’s early economy was sophisticated and globally connected, making it one of the wealthiest regions on Earth.

Illustration 2: Mughal Empire of India

However, the arrival of European colonial powers, especially the British East India Company in the 18th century, marked a profound shift. What was once a manufacturing and trading powerhouse became a supplier of raw materials and a captive market for British goods.

The colonial period saw the systematic deindustrialization of India’s traditional industries, such as the famous textile mills of Bengal, and the extraction of wealth that hindered economic progress for nearly two centuries. By the time India gained independence in 1947, its share of the global economy had dwindled to a mere 3%, a shadow of its former glory.

Illustration 3: British India led to India falling from making up 22.6% of the world economy in 1700 to 3.8% in 1952.

After independence, India embarked on a path shaped by the vision of Prime Minister Jawaharlal Nehru, who championed a socialist-inspired model of economic development. The state took control of key industries such as heavy manufacturing, banking, railways, and energy.

While this helped establish a basic industrial base, it also resulted in the notorious “License Raj,” a cumbersome system of permits and bureaucratic controls that stifled entrepreneurship and economic dynamism. For decades, India’s growth rate lingered at a modest 3 to 4 percent, a pace so slow it was mockingly dubbed the “Hindu rate of growth.

The turning point came in 1991 when a severe balance of payments crisis forced India to fundamentally rethink its economic model. Led by Finance Minister Manmohan Singh, the government embarked on sweeping reforms that dismantled import restrictions, reduced subsidies, and opened the economy to foreign investment. This liberalization unleashed a wave of economic activity that transformed India into a global player. The IT sector boomed, telecom networks expanded, pharmaceutical companies grew to global prominence, and financial markets developed rapidly. India’s economy accelerated, foreign reserves surged, and the nation gained credibility on the world stage.

The Structure of the Indian Economy

India’s economy is broadly divided into three main sectors: agriculture, industry, and services. Together, these sectors weave a complex and sometimes contradictory tapestry. While agriculture still employs the largest share of the workforce, roughly 43% of the population, it accounts for only about 20% of GDP.

Illustration 4: The Indian economy is complex like a tapestry

Industry contributes around a quarter of the GDP and employs about a quarter of the labor force. The services sector dominates the economy, representing more than half of the country’s GDP, yet employs only about a third of the workers. This structural imbalance highlights some of India’s greatest development challenges but also points to immense opportunities for growth and modernization.’

1. Industry and Manufacturing

Historically a late bloomer in manufacturing, India has increasingly turned its attention to industrial development. The government’s flagship initiative, “Make in India,” aims to expand the manufacturing sector’s share of GDP to 25 percent.

he automobile sector is one of the largest in the world, with companies like Tata Motors, Mahindra & Mahindra, bajaj auto, TVS motor company, Atul Auto and Maruti Suzuki producing millions of vehicles annually. As of 2023, India ranked as the fourth-largest automobile producer in the world, following China, United States and Japan. T

he sector accounts for approximately 7.1% of India’s GDP and employs over 37 million people directly and indirectly. As of April 2022, India’s auto industry is worth more than US$100 billion and accounts for 8% of the country’s total exports and 7.1% of India’s GDP.

Illustration 5: India is one of the world’s largest producers of tuk tuks

The pharmaceutical industry, often called the “pharmacy of the world,” manufactures 60 percent of the world’s vaccines and is a global leader in generic drugs. Heavy industries such as steel, cement, and chemicals are dominated by conglomerates like Tata Steel and Aditya Birla Group.

India is also carving a niche in emerging industries such as semiconductors, solar energy equipment, and electric vehicles, with states like Gujarat and Tamil Nadu competing fiercely to attract large factories and investment. Defense manufacturing is another growing priority, as India seeks to reduce its dependence on arms imports and develop indigenous capabilities.

Mining contributed to 1.75% of GDP and employed directly or indirectly 11 million people in 2021. India’s mining industry was the fourth-largest producer of minerals in the world by volume, and eighth-largest producer by value in 2009.

In output-value basis, India was one of the five largest producers of mica, chromite, coal, lignite, iron ore, bauxite, barite, zinc and manganese; while being one of the ten largest global producers of many other minerals.

Illustration 6: Rajesthan is one of the indian states with the most natural resources

Indian cement industry is the 2nd largest cement producing country in the world, next only to China. At present, the Installed Capacity of Cement in India is 500 MTPA with production of 298 million tonnes per annum. Majority of the cement plants installed capacity (about 35%) is located in the states of south India.

India surpassed Japan as the second largest steel producer in January 2019.The country’s steel sector benefits from abundant iron ore reserves, a large labor force, and strong government support through initiatives like “Make in India” and the National Steel Policy. As demand for steel rises both domestically and globally, India continues to expand its production capacity and export footprint.

Petroleum products and chemicals are a major contributor to India’s industrial GDP, and together they contribute over 34% of its export earnings. India hosts many oil refinery and petrochemical operations developed with help of Soviet technology such as Barauni Refinery and Gujarat Refinery, it also includes the world’s largest refinery complex in Jamnagar that processes 1.24 million barrels of crude per day.

By volume, the Indian chemical industry was the third-largest producer in Asia, and contributed 5% of the country’s GDP. India is one of the five-largest producers of agrochemicals, polymers and plastics, dyes and various organic and inorganic chemicals. Despite being a large producer and exporter, India is a net importer of chemicals due to domestic demands. India’s chemical industry is extremely diversified and estimated at $178 billion.

India is one of the largest producers and consumers of chemicals and fertilizers in the world, with the chemical industry contributing over 7% to the country’s GDP and ranking 6th globally in chemical production. At present, 57 large fertilizer units are manufacturing a wide number of nitrogen fertilizers. These include 29 urea-producing units and 9 ammonia sulfate-producing units as a by-product. Besides, there are 64 small-scale producing units of single super phosphate.

The fertilizer sector, vital for India’s agriculture, produced around 43.7 million tonnes of fertilizers in 2024–25, including urea, DAP, and complex fertilizers, supported by government subsidies and increasing adoption of nutrient-based fertilizers. The growing demand from agriculture, textiles, and pharmaceuticals continues to drive expansion in both sectors.

Illustration 7: India is one of the largest producers of dye in the world.

Furthermore, when it comes to transportation India is the third-largest domestic aviation market in the world, with passenger traffic reaching over 280 million in 2023. As of 2024, the country has 149 operational airports, up from 74 in 2014, and the government plans to expand this to 220 airports by 2030 under a 1 trillion Indian rupees infrastructure push.

India’s railways, contributing about 2% to the country’s GDP, transport over 8 billion passengers and 1.2 billion tonnes of freight annually, making it one of the world’s largest and busiest rail networks. The sector supports around 7 million jobs, both directly and indirectly, playing a crucial role in driving economic growth and connecting markets across the nation. With ongoing investments in modernization, electrification, and high-speed rail, Indian Railways is set to boost productivity and sustainability even further.

Illustration 8: Mumbai train station

India also has multiple ship building companies such as Cochin Shipyard, Hindustan Shipyard and Swan Defence and Heavy Industries, mainly produces ships for European, South American and African shipping companies. Cochin shipyard is the pioneer in autonomous electric propulsion ships.

2. Agriculture – The Paradox of Inida’s economy

Agriculture remains the cornerstone of India’s socio-economic landscape, deeply intertwined with the lives of over 40% of the population who depend on it for their livelihoods. Despite its declining share of around 16-17% in the country’s GDP, the sector is critical for ensuring food security, sustaining rural communities, and maintaining social stability across vast regions.

India proudly holds the title as the world’s largest producer of milk, pulses, and spices, and is among the top global producers of staples like rice, wheat, sugarcane, cotton, and a wide variety of fruits and vegetables, feeding over 1.4 billion people.

Yet, beneath this agricultural abundance lies a paradox: low productivity and fragmented landholdings often limit farmers’ incomes and economic resilience. Most farms are small, averaging less than 2 hectares, which constrains the adoption of advanced technology and efficient farming practices.

Additionally, frequent climate shocks, such as droughts, floods, and erratic monsoons, leave millions vulnerable and threaten crop yields year after year. Infrastructure challenges, including inadequate irrigation, poor storage facilities, and inefficient supply chains, further reduce farmers’ ability to maximize profits and reach larger markets.

Illustration 9: India is one of the largest producers of tea

Recognizing these challenges, India has embarked on a path to modernize agriculture by investing in better irrigation systems, promoting mechanization, improving rural roads and cold storage, and embracing digital technologies like satellite imaging and mobile apps to provide real-time information to farmers.

India’s agriculture and allied sectors remain a vital part of the economy, accounting for 18.4% of GDP and employing nearly 46% of the workforce, despite the sector’s shrinking share in overall economic output, from 52% in 1951 to around 15% in 2023.

The country boasts the largest arable land area in the world, ranking as a top global producer of milk, pulses, spices, rice, wheat, sugarcane, cotton, fruits, and vegetables. However, productivity challenges persist, with yields often only 30% to 50% of global best practices due to small landholdings, inadequate irrigation (only about 39% of cultivated land is irrigated), and infrastructure gaps in storage, roads, and markets. These issues limit farmers’ incomes and keep agricultural output below its full potential.

India is also a global leader in fisheries and aquaculture, ranking 3rd and 2nd respectively, providing livelihoods to millions, and exporting significant quantities of processed products like cashew kernels and milk. While the country produces roughly 316 million tonnes of foodgrains annually, stagnation in output and large post-harvest losses, up to one-third of production, highlight inefficiencies.

Government initiatives like the ₹1.2 trillion Accelerated Irrigation Benefit Programme aim to improve irrigation and infrastructure, but regulatory hurdles and market constraints continue to slow progress. Overall, India’s agriculture sector is a complex blend of immense scale, rich diversity, and urgent need for modernization to boost productivity and farmer prosperity.

Illustration 10: Indian women pounding rice, India is one of the world’s largest rice producers

However, progress has been uneven and often slowed by political sensitivities and social complexities. The massive farmer protests of 2020–21 underscored the deep-rooted concerns and emotional ties surrounding land rights, pricing, and market reforms. These protests highlighted how any attempt to transform India’s agricultural sector must carefully balance economic modernization with the protection of farmers’ livelihoods and rights.

Looking ahead, the future of Indian agriculture depends on successfully navigating this delicate balance, integrating technology and innovation while ensuring inclusivity and sustainability. With targeted reforms, climate-resilient farming practices, and strengthened rural infrastructure, India has the potential not only to feed its vast population but also to emerge as a global leader in sustainable agriculture.

3. Services – The Crown Jewel

The services sector has emerged as the undisputed engine of India’s economic growth, contributing a staggering over 50% of the country’s GDP, making it the largest sector in the Indian economy. From IT and software exports to financial services, healthcare, education, telecommunications, tourism, logistics, and more. the breadth and dynamism of this sector reflect India’s transition from a primarily agrarian economy to a global services leader.

Illustration 11: The city of Hyderabad is becoming a global hub for IT.

Cities like Bengaluru, Hyderabad, Gurugram, and Pune have become world-renowned hubs for IT, software development, business process outsourcing (BPO), and innovation, attracting investments from global tech giants and startups alike.

India’s Information Technology and Business Process Management (IT-BPM) sector alone generated over $250 billion in revenue in 2023, employing more than 5 million professionals, and contributing significantly to foreign exchange earnings.

Indian IT firms serve clients across the globe, from Silicon Valley startups to Fortune 500 corporations, delivering everything from cloud computing to AI solutions. Beyond tech, India’s financial services sector, anchored by robust public and private banks, insurance companies, fintech startups, and stock exchanges like NSE and BSE, plays a pivotal role in capital formation and investor confidence.

India’s telecom sector is a global giant, now the second-largest market in the world with over 1 billion phone subscribers and one of the lowest call tariffs due to intense competition. In FY 2024, telecom equipment production crossed ₹45,000 crore, with exports hitting ₹10,500 crore, driven by the booming smartphone manufacturing industry. India also ranks among the top three globally in internet users, and is the largest DTH television market by subscribers making digital connectivity a key pillar of its economic growth.

Equally significant is the rise of tourism, healthcare, education, retail, e-commerce, and digital services, all of which are rapidly expanding with the growing urban middle class and increasing internet penetration. The Unified Payments Interface (UPI) revolutionized digital transactions, processing billions of transactions monthly, and helped formalize vast segments of the economy. Meanwhile, the services sector has also become a major employment generator, especially in urban and semi-urban areas, offering opportunities in both high-skilled and low-skilled segments.

The government’s focus on initiatives like Digital India, Skill India, and Start-Up India further accelerates the services sector’s potential, promoting entrepreneurship, digital infrastructure, and employment. However, to sustain this momentum, India must address key challenges, such as improving ease of doing business, upskilling the workforce, enhancing service exports, and bridging the digital divide in rural areas.

In essence, the services sector is not just a component of India’s economy, it is its beating heart, transforming the country into a knowledge-based, innovation-driven powerhouse that is well on its way to becoming a major player in the global economic landscape.

Innovation and the Digital Revolution

India’s 63 million MSMEs (Micro, Small, and Medium Enterprises) contribute 35% to GDP, employ over 111 million people, and make up 40% of exports, earning their title as the “growth engines” of the economy. Though 90% are micro-enterprises with limited scale, 2023 saw a record 179 SME IPOs, showing rising investor interest. With continued policy support and reforms, MSMEs hold the key to tackling unemployment and driving inclusive growth.

India’s digital transformation has been nothing short of revolutionary. Central to this has been the Unified Payments Interface (UPI), a real-time digital payment system that processes billions of transactions monthly, outpacing even the combined digital payments of the US, China, and the EU. The Aadhaar biometric identification system has provided over 1.3 billion Indians with a unique digital identity, enabling unprecedented access to banking, government services, and welfare programs.

Together with the Jan Dhan-Aadhaar-Mobile (JAM) trinity, these innovations have democratized access to finance and services across vast rural and urban populations. The government’s Digital India initiative aims to further embed technology into governance, business, and daily life, while targeted programs such as Startup India and the Semiconductor Mission are propelling innovation and domestic manufacturing.

Furthermore, India’s youthful population is one of its greatest assets. With a median age of just 28.4 years, India is far younger than many developed countries whose median ages often exceed 40. Each year, approximately twelve million young people enter the labor market, creating both an opportunity and a challenge to generate sufficient employment. By 2030, India is expected to be home to seven megacities and more than 600 million urban residents, fueling demand for housing, infrastructure, transportation, and services.

Illustration 12: India’s population is very young something that can become its great asset.

The key to harnessing this demographic dividend lies in education and skills training to ensure that young Indians are productive contributors to the economy rather than unemployed or underemployed.

India’s cultural richness and heritage form a vital pillar of its economy. The country attracted more than 17 million tourists in 2023, contributing significantly to local economies.

Beyond the traditional pilgrimage and heritage tourism sectors, India’s global influence is bolstered by Bollywood, yoga, cuisine, cricket, and festivals that resonate worldwide. The Indian diaspora, numbering over 30 million people globally, acts as a powerful cultural and economic bridge, enhancing India’s soft power and international reputation.

Illustration 13: A Bollywood poster

Trade and Global Integration

India’s role in global trade continues to expand rapidly. As the world’s ninth-largest exporter of goods and sixth-largest importer, India’s export basket includes refined petroleum, gems and jewelry, pharmaceuticals, automobiles and parts, and software services. The United States, China, the United Arab Emirates, the European Union, and ASEAN nations are India’s most significant trading partners.

India is actively negotiating free trade agreements with major economies like the UK and the EU and is building regional supply chains to reduce reliance on China and enhance economic resilience. On the global stage, India positions itself as a leading voice for the developing world, championing issues such as debt relief, food security, and climate action, especially during its G20 presidency in 2

Credit Score

India currently holds a sovereign credit rating of “BBB-” with a stable outlook from S&P and Fitch, and a “Baa3” from Moody’s, both of which are the lowest investment-grade ratings. These ratings indicate that India is a relatively safe destination for investment, but with moderate credit risk. The scores reflect a balance between India’s strong long-term growth prospects and structural economic challenges such as a high fiscal deficit, significant public debt, and dependency on imported energy.

The rating agencies acknowledge India’s resilient and diversified economy, large domestic market, improving infrastructure, and digital innovation as strengths. India’s track record of stable democratic governance, reforms in taxation (like GST), and emphasis on infrastructure and ease of doing business further support its rating. However, concerns remain over fiscal discipline, with the government debt-to-GDP ratio hovering around 83%, and recurring fiscal deficits above 5%, driven by subsidies, welfare schemes, and lower tax revenues.

Despite global economic uncertainties, India’s strong GDP growth, estimated at around 6–7% annually, even during volatile periods, continues to reinforce investor confidence. Many experts believe that with continued reforms, improved tax collection, and responsible fiscal management, India could see a credit upgrade in the coming years, which would lower borrowing costs and attract more foreign investment.

Challenges and contradictions

Despite its impressive rise, India faces deep-seated challenges. Income inequality is stark, with the richest one percent controlling more than 40% of the nation’s wealth. Structural issues such as unemployment. especially among youth and graduates, remain unresolved. While India has made strides in reducing corruption and improving ease of doing business, bureaucratic inertia and red tape still hinder many entrepreneurs.

Environmental problems loom large as well. Air pollution in cities frequently reaches hazardous levels, water scarcity threatens agriculture and urban centers, and climate change presents an existential risk to development gains. Public debt, while moderate compared to many developed nations, is rising and will require careful fiscal management.

Illustration 14: Ambani tower in India highlighting the difference between rich and poor in the country.

India’s Global Ambitions

Looking forward, India has set ambitious goals to become a $5 trillion economy by 2027 and to join the ranks of the world’s top three economic powers by 2050. The government’s vision of “Viksit Bharat,” or Developed India, aims for transformational progress by the centenary of independence in 2047.

Priority sectors include renewable energy, where India is already a global leader in solar power and has pledged to reach net-zero carbon emissions by 2070. Defense manufacturing, advanced technologies such as artificial intelligence and quantum computing, biotechnology, and infrastructure development are all central to India’s future growth plans.

Massive investments in freight corridors, expressways, and ports are underway to improve logistics and connect the vast country more efficiently.

Conclusion

India’s economy embodies a unique paradox. It is ancient and modern, fast-growing yet uneven, chaotic yet bursting with creative energy. Unlike the more streamlined and centralized economies of Germany or China, India’s democratic capitalism is messy and vibrant, shaped by millions of individual decisions, countless startups, and an energetic population.

Illustration 15: India is one of the fastest growing economies in the world.

Its rise is not just an economic story but a human one, about a nation harnessing its vast potential, striving to lift hundreds of millions out of poverty, and aiming to reshape the global economic order. As smartphones proliferate in small towns, solar panels spread across deserts, and coding campuses thrive in Bangalore and Hyderabad, India is writing a new chapter in the story of global growth.

India’s economy is a dynamic blend of traditional strength and modern innovation, driven by a powerful services sector, a vast and evolving agricultural base, and a rapidly growing industrial and manufacturing ecosystem. With a young population, expanding digital infrastructure, and consistent GDP growth averaging 6–7%, India is well-positioned to become one of the world’s leading economic powers. However, to fully unlock its potential, the country must address key challenges like unemployment, low agricultural productivity, infrastructure gaps, and fiscal discipline, while continuing to invest in reforms, technology, and human capital.

Canadian Solar Inc. is one of the largest and most established solar energy companies in the world. It has made significant contributions to the global transition toward renewable energy, specifically solar power. With a presence in over 20 countries, Canadian Solar has successfully integrated itself into both the manufacturing of solar photovoltaic (PV) products and the development of solar projects. In this article, we will explore the history, operations, competitive positioning, financials, the future prospects of Canadian Solar and of course make a comprehensive analysis of the stock of Canadian Solar.

History and Founding

Canadian Solar was founded in 2001 by Dr. Shawn Qu, a former University of Toronto researcher with a background in electrical engineering. Dr. Qu, originally from China, started the company in Ontario, Canada, with the goal of providing high-performance solar modules at competitive prices. The company’s initial focus was on manufacturing solar cells and modules, and its breakthrough came with its focus on high efficiency and the development of advanced technologies in the solar industry.

The decision to base the company in Canada was a strategic move, given the country’s growing interest in clean energy and environmental sustainability. However, Canadian Solar’s roots were international, as Dr. Qu leveraged relationships in China for access to affordable manufacturing resources. The company quickly expanded from its Canadian base and set up large-scale manufacturing operations in China, where it remains one of the leading solar module manufacturers today.

Canadian Solar’s commitment to innovation and sustainability has allowed it to grow from a small, niche manufacturer to a global leader in solar energy. The company’s products are now used in residential, commercial, and utility-scale solar projects around the world, making Canadian Solar a key player in the global energy transition.

Illustration 1: Canadian Solar logo with sun and rays symbolizing commitment to solar power.

Operations and Products

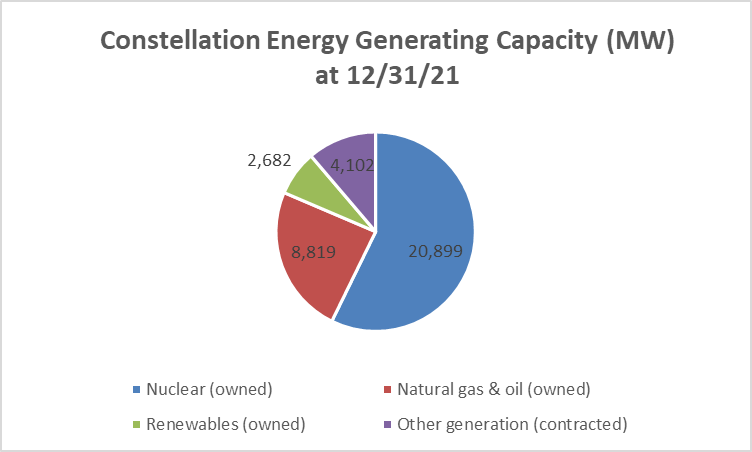

Canadian Solar operates in two major segments: Solar Module Manufacturing and Solar Power Projects.

Solar Module Manufacturing Canadian Solar produces a wide range of photovoltaic (PV) products, including solar modules, inverters, and energy storage systems. Their solar panels are among the most efficient on the market, with varying products designed for different types of consumers, ranging from residential to large-scale commercial and utility installations. The company uses advanced technology such as PERC (Passivated Emitter and Rear Cell) to ensure high efficiency and durability of their modules.

Solar Power Projects Beyond manufacturing, Canadian Solar is actively involved in the development, financing, and operation of solar power projects globally. This segment includes utility-scale solar farms, distributed solar energy systems for commercial and industrial clients, and energy storage solutions.

Canadian Solar has completed over 10 GW of solar projects worldwide, cementing its position as a leading solar energy provider. The company focuses on end-to-end solar solutions, offering customers everything from project development to system integration, operation, and maintenance.

In addition to these, Canadian Solar has made significant strides in the energy storage market. As the world shifts towards renewable energy, energy storage solutions are seen as a key enabler for balancing intermittent power generation from solar and wind energy. Canadian Solar’s energy storage division, which works in tandem with their solar projects, provides customers with grid-independent solutions that help store excess energy for later use.

Revenue Breakdown

The revenue breakdown of Canadian Solar is as follows:

1. Solar Module Manufacturing: This segment represents the largest portion of Canadian Solar’s revenue, contributing approximately 60-70%. The company’s solar modules are sold to both residential and commercial customers and are used in utility-scale projects. This portion of the business continues to grow as demand for solar energy increases globally, driven by favorable government policies, falling solar costs, and rising environmental concerns.

2. Solar Power Projects: The company’s solar power projects segment accounts for around 25-35% of its revenue. This portion includes the sale of solar power plants, as well as ongoing income generated from the operation of these plants. Over the years, Canadian Solar has managed to increase its share of revenue from projects, reflecting the growing demand for large-scale solar farms and distributed generation systems.

3. Energy Storage and Other Products: Although a smaller segment, energy storage systems and other ancillary products are becoming an increasingly important part of Canadian Solar’s portfolio. This segment contributes roughly 5-10% of the company’s total revenue.

Illustration 2: Energy Storage is quickly becoming a growing sector for Canadian Solar.

Canadian Solar has also been successful in managing costs and improving operational efficiency. The company’s gross margin has steadily improved due to its focus on high-efficiency products and scaling its manufacturing operations.

Key Competitors

Canadian Solar operates in a very highly competitive market. Its key competitors include:

First Solar (FSLR): A US-based solar energy company, First Solar is one of the leading manufacturers of thin-film solar modules. Unlike Canadian Solar, which primarily produces crystalline silicon modules, First Solar specializes in cadmium telluride (CdTe) technology. First Solar is known for its utility-scale solar projects, similar to Canadian Solar’s project development segment.

JinkoSolar (JKS): Another Chinese solar giant, JinkoSolar is one of the largest manufacturers of solar panels globally. JinkoSolar’s strength lies in its focus on technology, with an emphasis on increasing panel efficiency and reducing costs. The company’s global footprint is comparable to Canadian Solar’s, and its competitive pricing makes it a formidable rival.

Trina Solar (TSL): Trina Solar is another major Chinese player in the solar market. Like Canadian Solar, it operates in both module manufacturing and project development. Trina Solar has a strong presence in Europe, the Americas, and Asia.

LONGi Green Energy (601012.SS): LONGi is one of the largest manufacturers of monocrystalline silicon solar products. With a focus on technology and efficiency, LONGi competes directly with Canadian Solar in the module manufacturing market.

SunPower (SPWR): Based in the United States, SunPower is a major player in both residential and commercial solar installations. SunPower differentiates itself by offering premium solar products, while Canadian Solar offers a broader range of modules for different market segments.

To sum up, the solar power market is highly competitive with many competitors to challenge Canadian Solar.

Market Position and Competitive Advantages

Despite very high competion Canadian Solar holds a competitive edge in several areas:

Global Reach: With manufacturing facilities in China, Canada, and other parts of the world, Canadian Solar has a robust global supply chain and can cater to customers in diverse markets. Its presence in the Americas, Europe, and Asia ensures that it remains competitive in the global solar market.

Innovation and Technology: Canadian Solar places a strong emphasis on research and development (R&D). The company consistently strives to improve the efficiency and durability of its solar panels, which has helped it maintain its competitive edge. Canadian Solar is at the forefront of solar cell and panel technology, incorporating advanced technologies like PERC and bifacial modules.

Illustration 3: Canadian Solar’s is well known for being invested in research and development.

Cost Leadership: One of the key drivers behind Canadian Solar’s success is its ability to maintain a competitive price point while offering high-quality products. By leveraging economies of scale and low-cost manufacturing in China, Canadian Solar can keep its prices lower than many competitors while maintaining margins.

Comprehensive Solutions: Unlike some competitors that focus primarily on module manufacturing, Canadian Solar offers a comprehensive solution, including project development and energy storage. This ability to offer turnkey solutions, from manufacturing to operation and maintenance, is a significant advantage in attracting large-scale customers.

Future Outlook

Looking ahead, Canadian Solar is well-positioned to continue its growth. The global transition to renewable energy is accelerating, with solar energy at the forefront. The company’s strong brand, technological innovation, and global footprint provide a solid foundation for its future growth. Canadian Solar is also well-positioned to benefit from government incentives and policies aimed at promoting renewable energy adoption.

With increasing demand for solar energy, growing interest in energy storage, and continued advancements in panel technology, Canadian Solar is expected to remain a leader in the solar industry.

Furthermore, the company’s expansion into emerging markets like India, Africa, and Latin America presents significant growth opportunities.

Stock Analysis

In this section we will analyze Canadian Solar’s stock to see if it is a good stock to buy or not. Our philosophy is value investing meaning that we try to find good quality companies that are undervalued. However, we will give a holistic overview so all kind of investors with different philosophies can judge the stock for themselves.

Revenue and Profits

To determine a company’s worth and if it is worth investing in, the company’s revenue and profits are a natural starting point to analyze. It should never bee forgotten that a stock represents a company just like the small businesses in your home town. If someone asked you if you want to buy their company, the first question would naturally be how much the company makes and the same question when trying to analyze if a company registered in the stock exchange is worth buying.

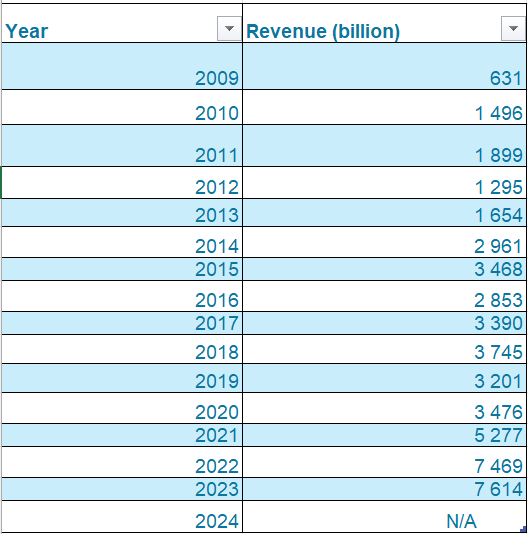

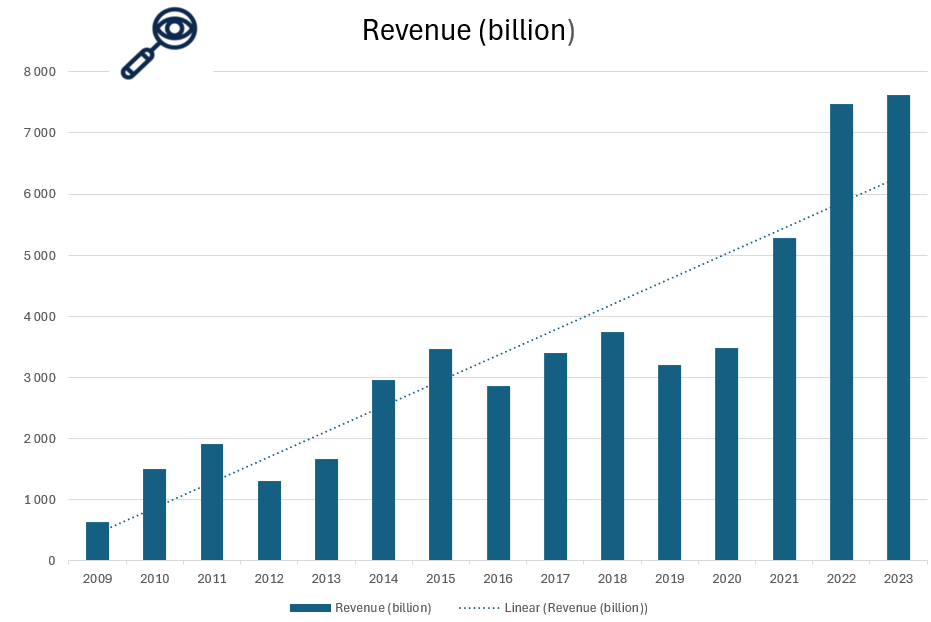

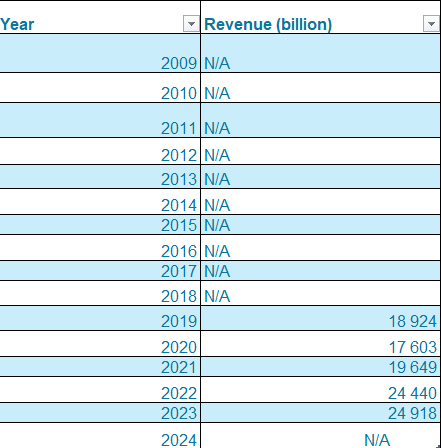

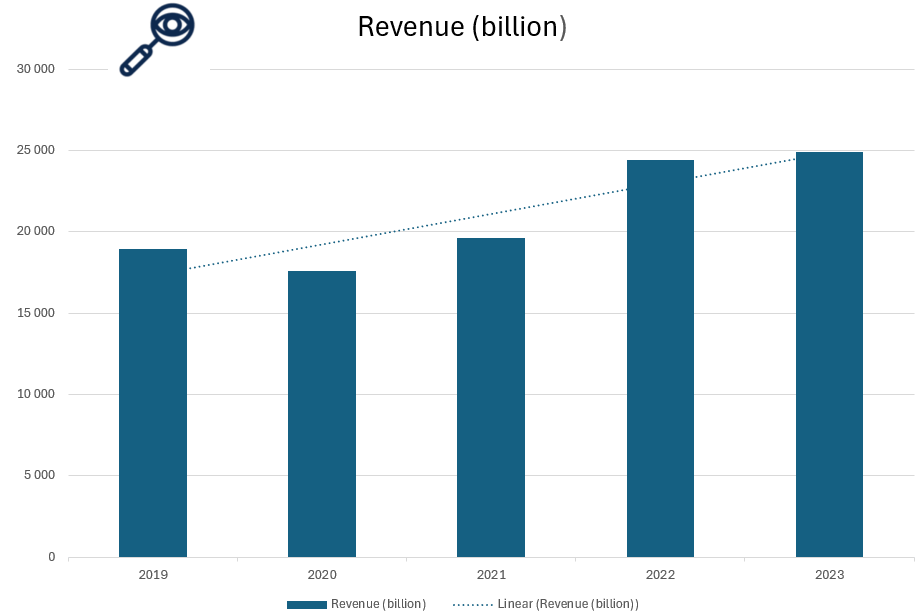

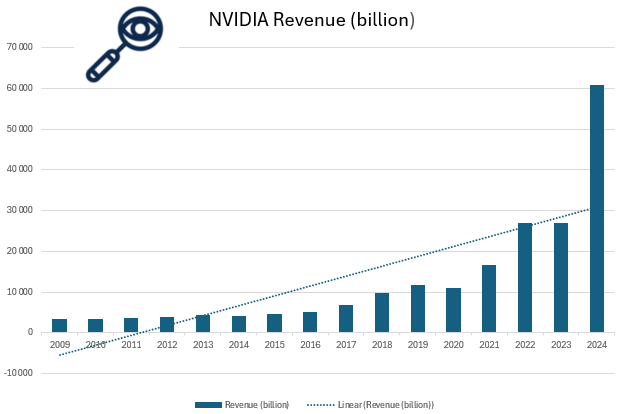

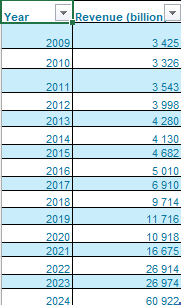

Illustration 4 and 5: Revenue of Canadian Solar from 2009 to 2023.

As seen in Illustrations 4 and 5, Canadian Solar’s revenue has been increasing over the long term, particularly in recent years. This growth is driven by rising global demand for solar energy, increased module shipments, and expansion into energy storage and project development. Additionally, favorable government policies and renewable energy commitments continue to fuel sales, positioning the company for sustained growth.

However, despite this overall upward trend, Canadian Solar’s revenue growth has been inconsistent. As shown in Illustrations 4 and 5, there have been years—such as 2012, 2016, and 2019—where revenue declined. This volatility is partly due to intense competition in the solar industry, fluctuating market conditions, and policy shifts affecting demand. For investors, this inconsistency raises concerns, as it suggests that Canadian Solar may not deliver steady revenue growth year after year, making it a potentially riskier investment compared to companies with more predictable financial performance.

Even though revenue growth has been inconsistent, the long-term trend remains upward. Considering the rising global demand for energy, the increasing popularity of solar power, and the momentum of the green energy transition, Canadian Solar is well-positioned for future growth. These factors, combined with the company’s expanding product offerings and global presence, suggest a promising outlook despite short-term volatility.

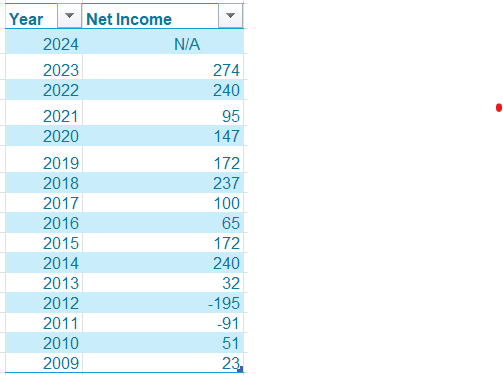

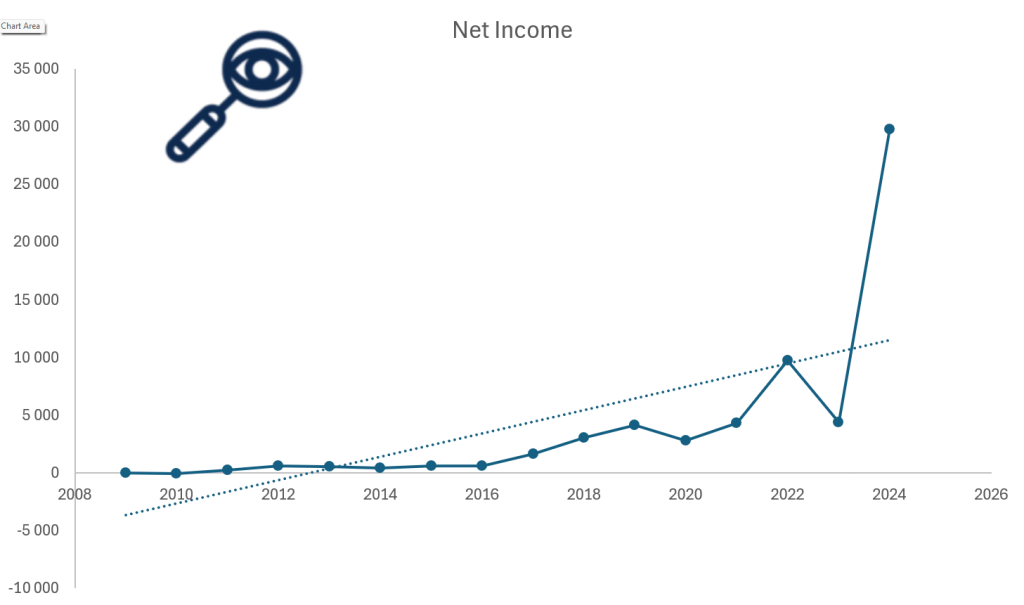

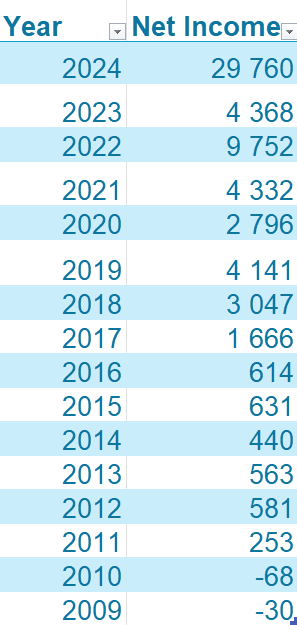

Illustration 6 and 7: Net Income of Canadian Solar from 2009 to 2023.

Net income is a crucial metric to evaluate when determining whether a company is a worthwhile investment. It represents a company’s net profit or loss after accounting for all revenues, income items, and expenses, calculated as Net Income = Revenue – Expenses.

As seen in Illustrations 6 and 7, Canadian Solar’s net profit has shown a slight upward trend but has mostly remained relatively flat with fluctuations since 2014, peaking around 250. This inconsistency is a red flag for potential investors, as it indicates that despite growing revenue, the company has struggled to achieve steady profit growth. Factors such as pricing pressure, industry competition, and fluctuating costs may be limiting profitability, making it difficult for investors to rely on sustained earnings growth. When investing in a company, increasing profits is one of the most—if not the most—important factors for investors. However, Canadian Solar has struggled to achieve consistent profitability, as its net income has remained relatively stable over the years despite growing revenue. This lack of sustained profit growth raises concerns about the company’s ability to improve margins and generate higher returns for shareholders in the long run.

Revenue breakdown

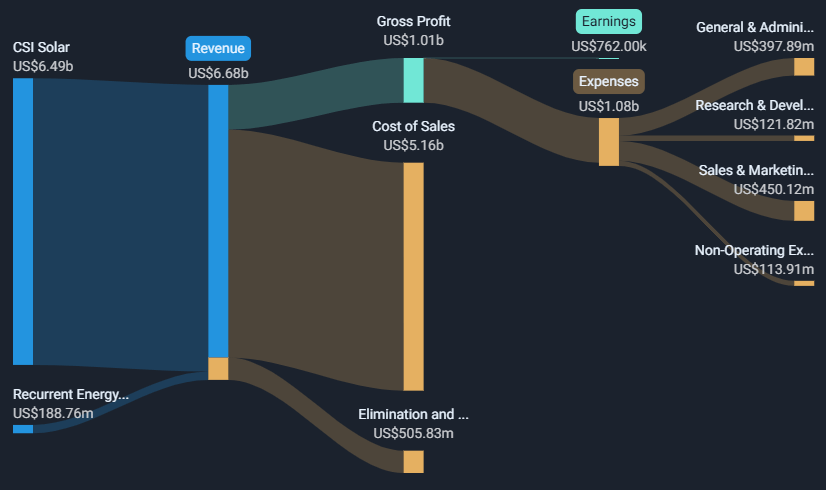

Illustration 8: Revenue Breakdown for Canadian Solar

As seen in Illustration 8, Canadian Solar is a pure-play solar energy company, generating all its revenue from the solar industry. This makes it an ideal investment opportunity for those seeking direct exposure to the solar sector. However, for investors looking for diversification within the broader utility sector, Canadian Solar may not be the best fit, as it lacks revenue streams from other energy sources or utility-related businesses.

Additionally, Illustration 8 highlights that the cost of sales in the solar energy industry is significantly high, which consumes a large portion of Canadian Solar’s revenue. On top of that, the company allocates substantial funds toward R&D, administration, and marketing, further limiting its net profit. As a result, despite strong revenue figures, the company’s actual profitability remains relatively low, which could be a concern for investors focused on earnings growth.

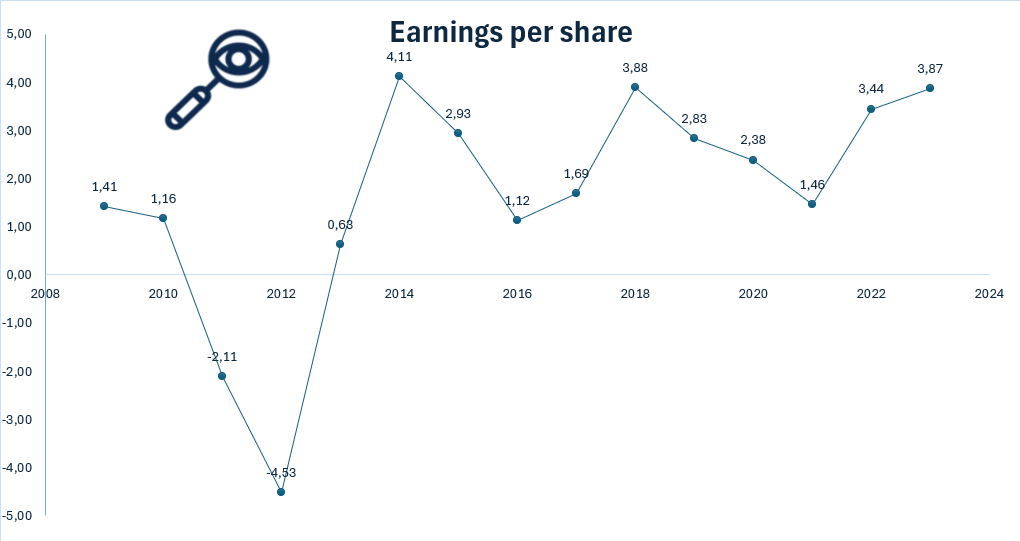

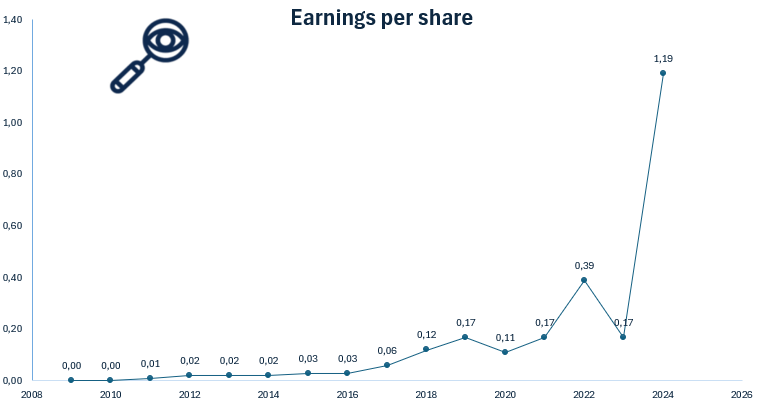

Earnings per shar (EPS)

Earnings Per Share (EPS) is a key financial metric that measures a company’s profitability on a per-share basis. It indicates how much profit a company generates for each outstanding share of its stock, and is used o assess a company’s financial health, profitability, and potential for growth. In other words this metric can tell us how profitable the business is,

Illustration 9: Earnings per share for Canadian Solar from 2009 to 2023.

The EPS figure itself isn’t the primary focus for value investors—it can be 0.2 or 10, but what truly matters is the company’s ability to generate consistent earnings growth. A steadily increasing EPS over time signals strong financial health, profitability, and long-term value creation.

Canadian Solar’s earnings per share (EPS) performance from 2009 to 2023 presents a mixed picture for investors. While the company has demonstrated resilience and growth in revenue over the long term, its EPS has been highly volatile, with significant fluctuations rather than a consistent upward trend. Periods of strong earnings, such as in 2014, have been followed by years of weaker performance, making it difficult for investors to predict steady profit growth. This inconsistency can be a red flag for long-term investors who prioritize stable and growing earnings, as it suggests that Canadian Solar’s profitability is sensitive to external factors like pricing pressure, raw material costs, and government policies.

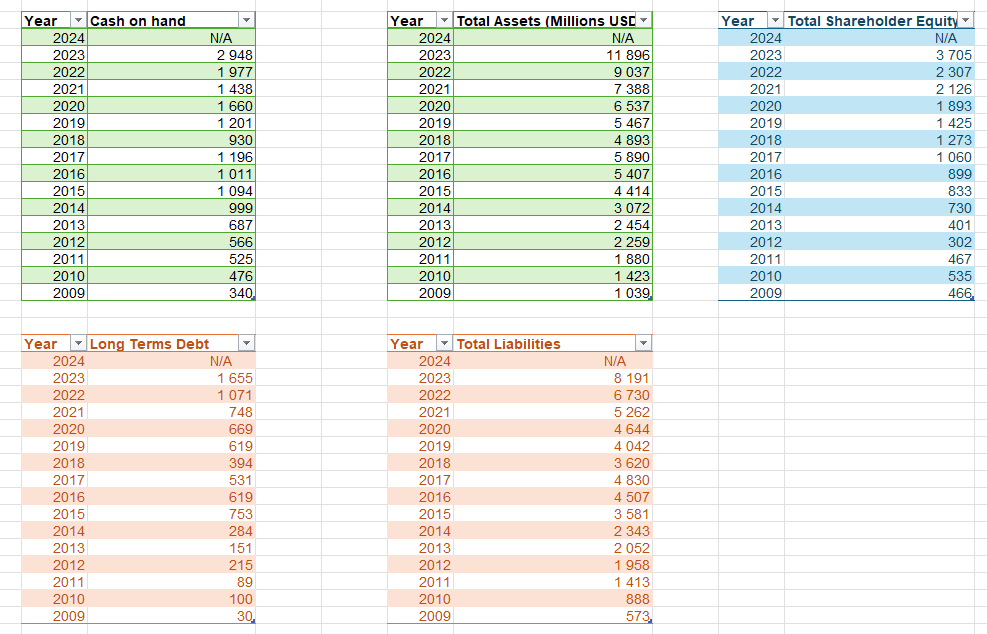

Assets and Liabilities

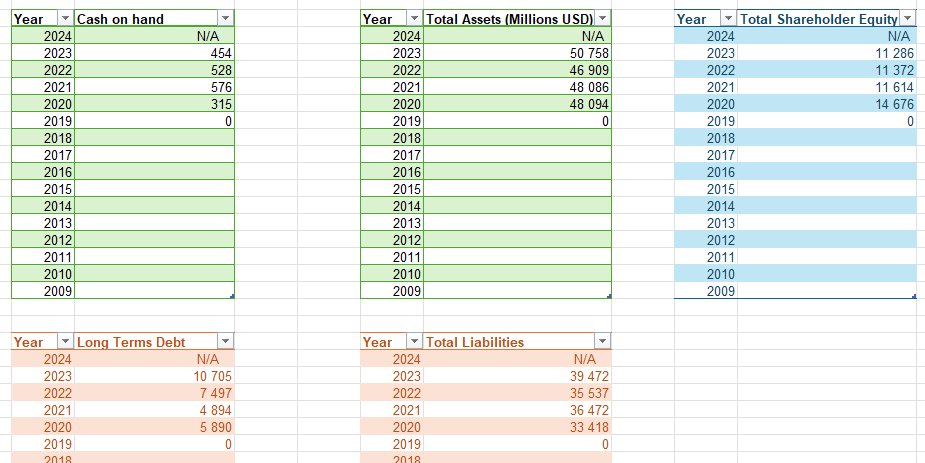

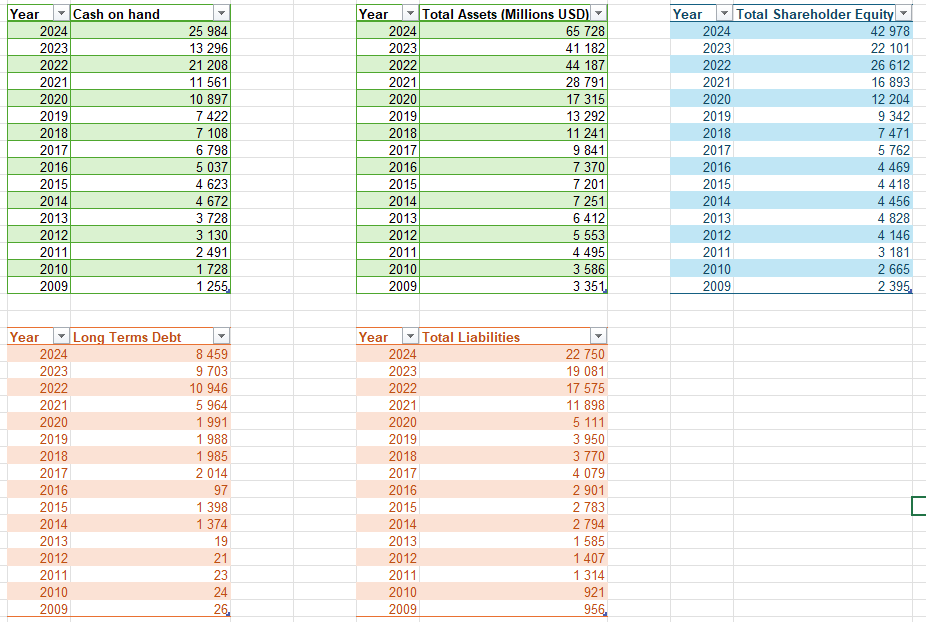

Illustration 10 and 11: Assets, Liabilities and Total Shareholder Equity for Canadian Solar from 2009 to 2023.

When evaluating a company as a potential investment, understanding its assets and liabilities is crucial. If a local business owner offered to sell their shop to you, one of the first questions—after determining its profitability—would be about its equity and assets. The same principle applies when assessing publicly traded companies like Dominion Energy.

As shown in Illustrations 10 and 11, Canadian Solar has a substantial asset base, totaling $11.9 billion in 2024. This steady asset growth over time is a positive sign, indicating that the company is expanding its operations, investing in new technologies, and strengthening its market position. A growing asset base often reflects a company’s ability to scale its business, acquire new projects, and improve its production capacity, which is particularly important in the highly competitive solar energy industry.

At the same time, Canadian Solar’s total liabilities have also increased significantly, rising from $573 million in 2009 to $8.2 billion in 2024. While such a sharp increase in debt might raise concerns for some investors, it is not necessarily a red flag given the nature of the solar energy business. Solar companies typically operate in a capital-intensive environment where they must secure substantial financing to fund large-scale projects, develop infrastructure, and maintain their competitive edge. Debt financing is often necessary for expanding solar farms, increasing manufacturing capacity, and advancing energy storage solutions, all of which contribute to long-term growth.

The key factor for investors is whether Canadian Solar can effectively manage its debt while maintaining strong revenue and profitability. If the company can generate consistent cash flow and sustain high demand for its products and services, its rising liabilities may not be a major issue. However, if debt levels continue to grow faster than revenue or profits, it could indicate financial strain, making it important for investors to monitor the company’s ability to service its obligations while maintaining profitability.

The cash on hand for Canadian Solar is a green flag for potential investors, as the company has $2.9 billion in readily available cash as of 2023. This strong cash reserve provides the company with flexibility and liquidity, enabling it to navigate market fluctuations, invest in new projects, and meet its short-term financial obligations without relying heavily on external financing.

Additionally, Canadian Solar’s long-term debt of $1.65 billion in 2023 is significantly lower than its available cash, which is a positive sign for investors. This indicates that the company has a solid financial cushion and is not overly reliant on debt to fund its operations. It suggests that Canadian Solar is in a strong position to manage its liabilities, fund future growth, and weather economic downturns without significant financial strain. This balance between cash and debt is reassuring for investors, as it reflects financial stability and prudent management of resources.

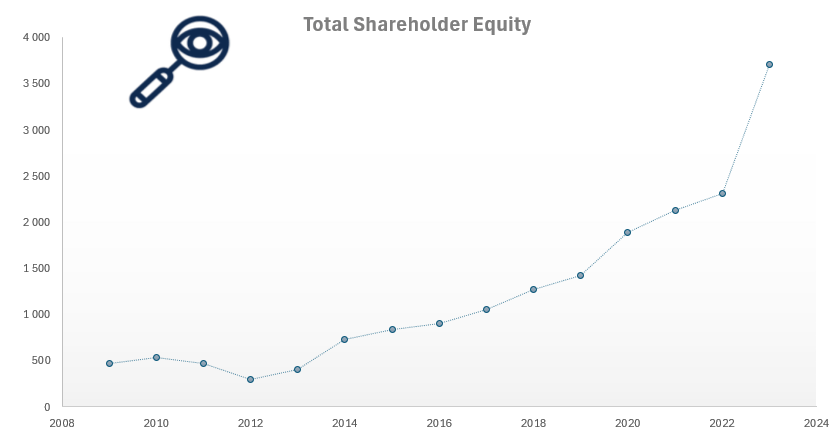

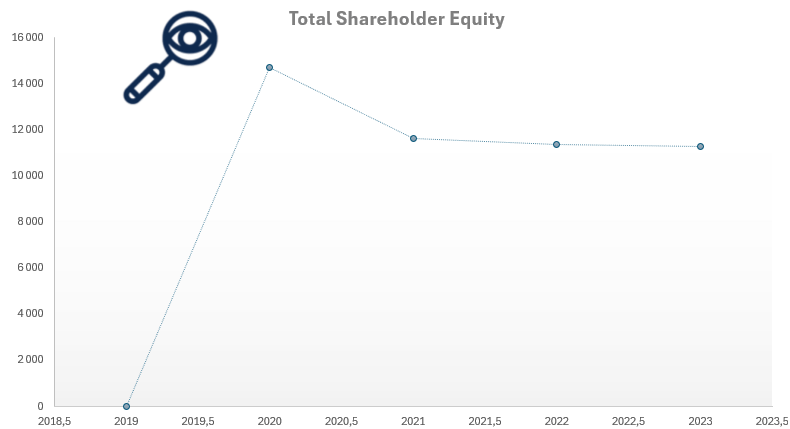

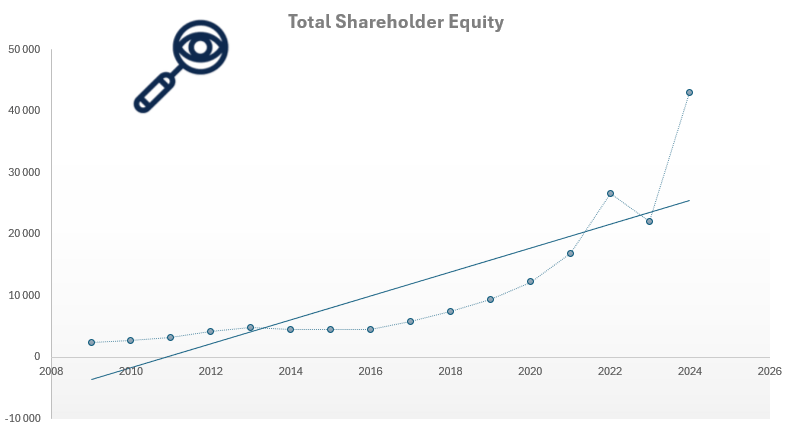

As seen in Illustration 11, Total Shareholder Equity—calculated as total assets minus total liabilities—has consistently grown over the past 14 years. This is a positive indicator for potential investors, as it suggests that Canadian Solar is building value over time rather than eroding its financial foundation. A steadily increasing shareholder equity indicates that the company’s assets are growing at a faster rate than its liabilities, which is a green flag for financial health. This trend suggests that Canadian Solar is successfully expanding its operations while maintaining a solid balance sheet. Additionally, rising equity provides a buffer against financial downturns, making the company more resilient in times of economic uncertainty. However, investors should also consider how this growth is achieved—whether through profitable operations or increased debt financing—to fully assess the sustainability of this trend.

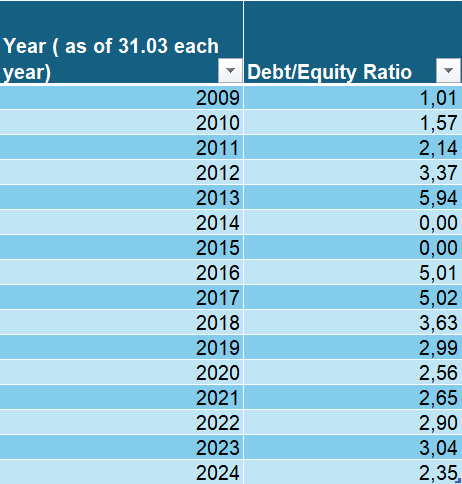

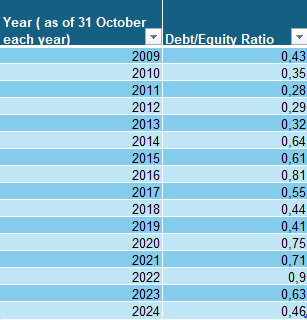

Debt to Equity Ratio

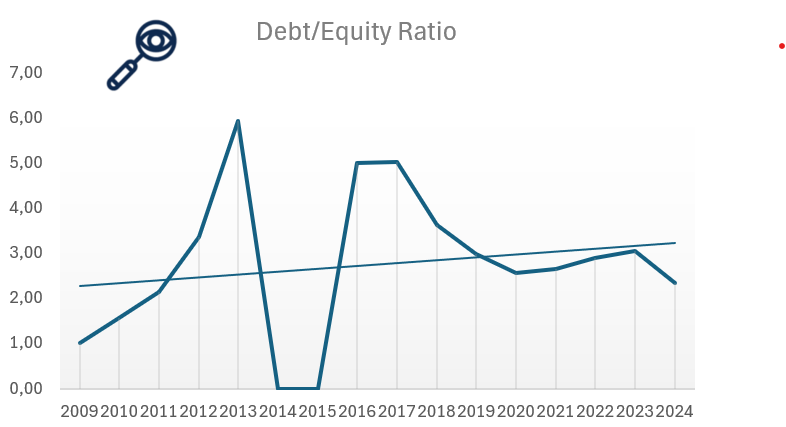

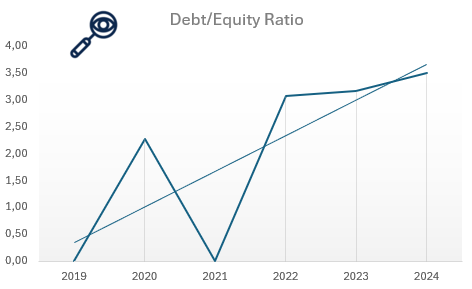

Illustration 12 and 13: The Debt to Equity ratio of Canadian Solar from 2009 to 2024.

The Debt-to-Equity (D/E) ratio is an important financial metric for assessing Canadian Solar’s financial leverage and risk. It compares the amount of debt the company uses to finance its operations relative to its shareholder equity. A high D/E ratio suggests that the company relies more heavily on debt to fuel growth, which could increase financial risk, especially during economic downturns when managing debt obligations becomes more challenging. In contrast, a lower D/E ratio indicates that Canadian Solar is primarily financed through equity, reducing financial risk but potentially limiting its ability to rapidly expand.

In recent years, Canadian Solar has maintained a relatively high D/E ratio, reflecting its reliance on both debt and equity financing to support its operations. This is typical for companies in the solar industry, as they often need to take on debt to fund large-scale projects, infrastructure, and expansion into new areas like energy storage. However, while leveraging debt is common in the sector, investors should remain cautious and monitor Canadian Solar’s ability to manage its increasing debt load. A high D/E ratio, particularly during periods of rising interest rates or market volatility, can place pressure on profitability and financial stability.

As of 2023, Canadian Solar’s D/E ratio reached nearly 6, and it was also high in 2016 and 2017, exceeding 5. While the company has made strides in reducing its debt and increasing equity over time, its D/E ratio remains substantially higher than the level recommended by investors like Warren Buffett, who prefers a ratio below 0.5. This suggests that while the company has made progress, Canadian Solar still carries a significant debt burden that investors should carefully assess to ensure it does not hinder long-term growth or financial health.

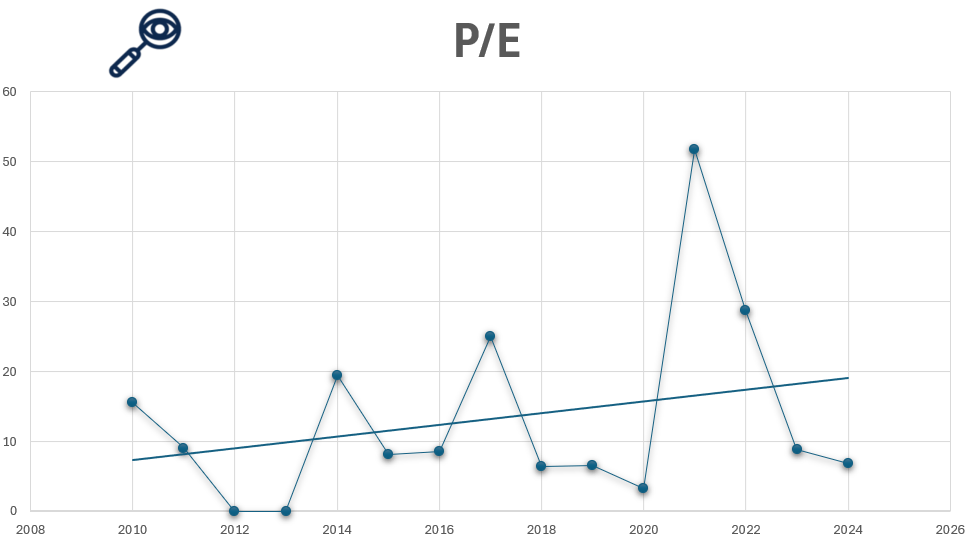

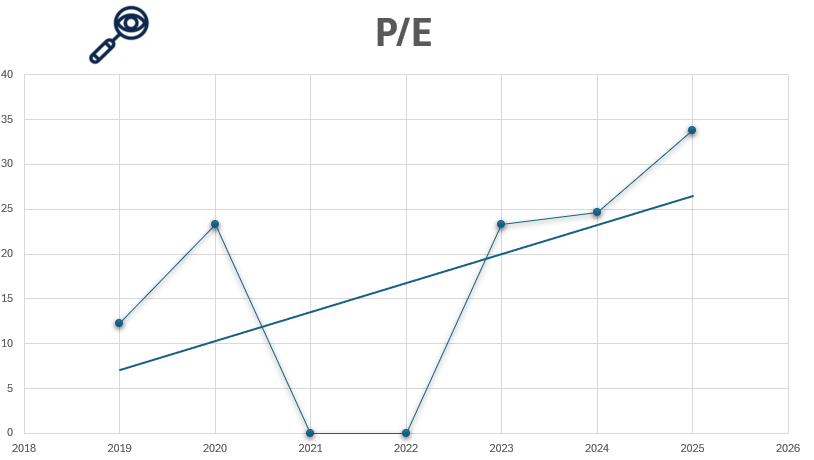

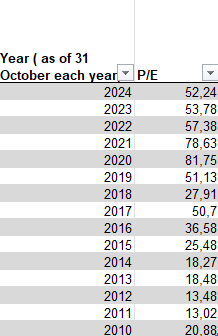

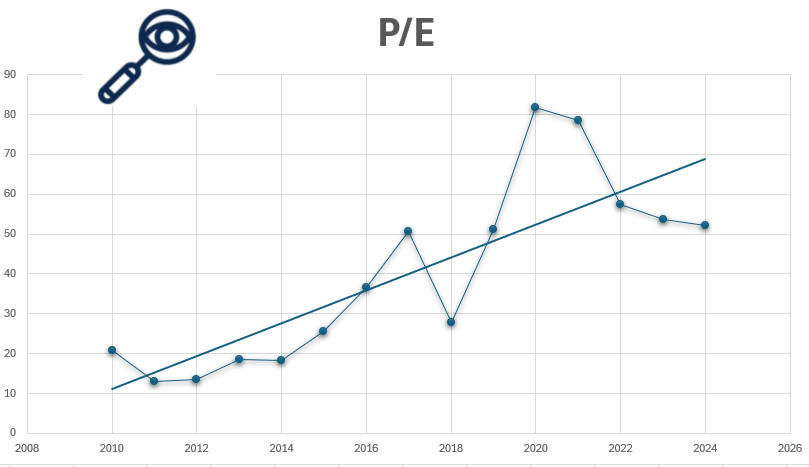

Price to earnings ratio (P/E)

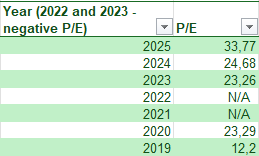

Illustration 14 and 15: The price to earning ratio for Canadian Solar from 2010 to 2024. The P/E ratio was negative and/or not available for 2012 and 2013.

For value investors, one of the most critical metrics when evaluating Canadian Solar’s stock is the price-to-earnings (P/E) ratio, as it helps assess whether the company is undervalued or overvalued. Even if a company has strong financials, purchasing its stock at a high price can lead to poor returns. For example, imagine a business generating solid profits of $1 million per year. If the owner offers to sell you the business for just $1, it would be an incredible deal. But if the owner asks for $1 trillion, even though the business is profitable, the price would be absurdly overvalued. The stock market works similarly—companies can be priced cheaply on some days and excessively expensive on others.

Warren Buffett, a legendary value investor, typically considers stocks with a P/E ratio of 15 or lower as “bargains.” A high P/E ratio suggests that investors are paying a premium for the company’s earnings, expecting significant growth. However, this also indicates that the stock is expensive relative to its earnings, which can be a red flag for value investors. Canadian Solar’s P/E ratio has fluctuated widely over the years. For example, it was in bargain territory at 4.93 in 2011, before reaching a strongly overpriced level of 62.2 in 2021. However, with the current P/E ratio of 29.90 at 16 February 2025, Canadian Solar’s stock can be seen as fairly priced, meaning it is neither undervalued nor an ideal investment for value investors seeking a strong bargain.

The strongly fluctuating prices for Canadian Solar indicates that the company’s stock price is volatile relative to its earnings, and signal uncertainty in the market or changing investor expectations about future growth. For potential investors the fluctuating prices gives them the opportunity to buy the stock at bargain price, but they should be very careful not buy at the top.

Dividend

Canadian Solar does not currently offer a dividend, focusing instead on reinvesting its profits into growth initiatives, including expanding solar projects and developing energy storage solutions. This approach is common for growth-focused companies, especially in the renewable energy sector, where significant capital is needed for expansion.

While Canadian Solar doesn’t provide regular income through dividends, its strategy of reinvestment can be appealing to growth investors looking for long-term capital appreciation rather than immediate returns. However, the lack of dividends may be a red flag for income-focused investors who rely on steady income from their investments. This strategy could also limit some investor interest, especially those seeking consistent payouts.

To summarize:

✅ Green Flag:

Growth Potential: By reinvesting profits, Canadian Solar is positioning itself for long-term growth in the rapidly expanding solar and renewable energy sectors.

Capital Allocation: The company prioritizes strategic investments in projects and innovation over dividend payouts.

🚩 Red Flag:

No Dividend: The lack of dividends may deter income-seeking investors, as Canadian Solar reinvests all profits rather than distributing earnings to shareholders.

Insider Trading

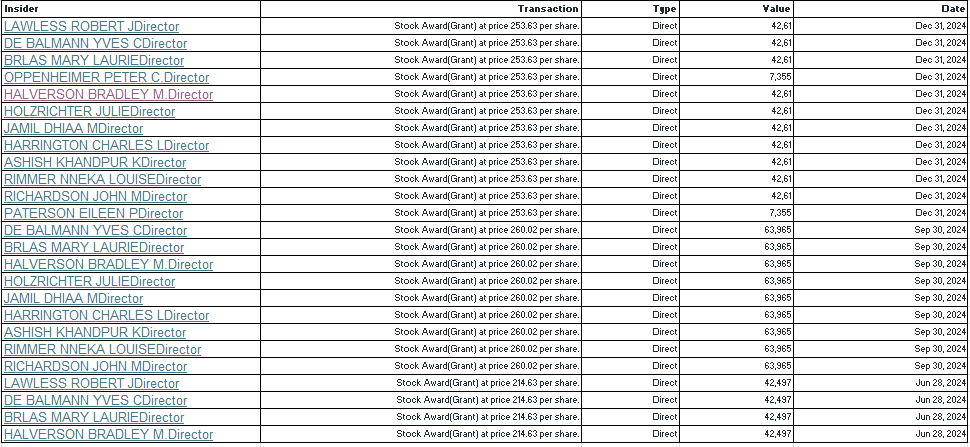

A key metric to consider when evaluating Canadian Solar as an investment isinsider trading activity, specifically whether company insiders have been buying or selling shares in the past year. It’s important to focus on who is making these transactions, with particular attention to directors, as their actions often provide more insight into the company’s future prospects than those of officers.

As shown in recent data, there has been no insider selling at Canadian Solar. This is a green flag for investors, as it suggests that insiders have confidence in the company’s future performance and are holding on to their shares, rather than liquidating them.

Other Company info

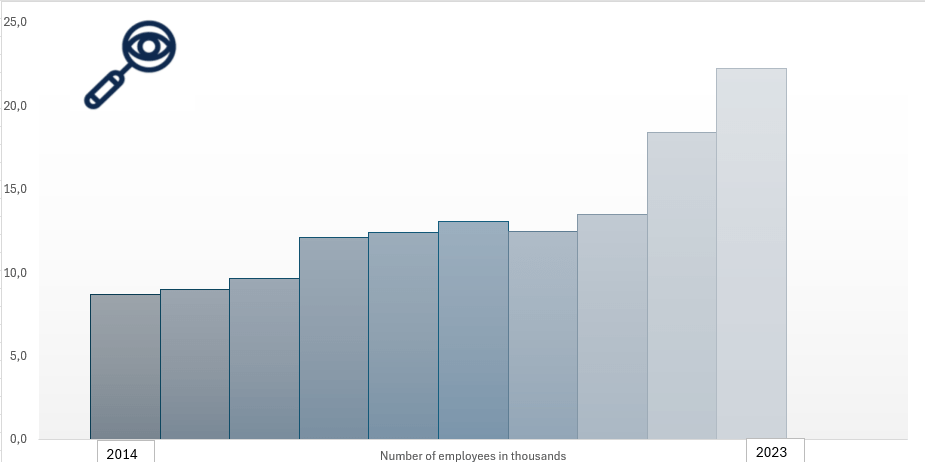

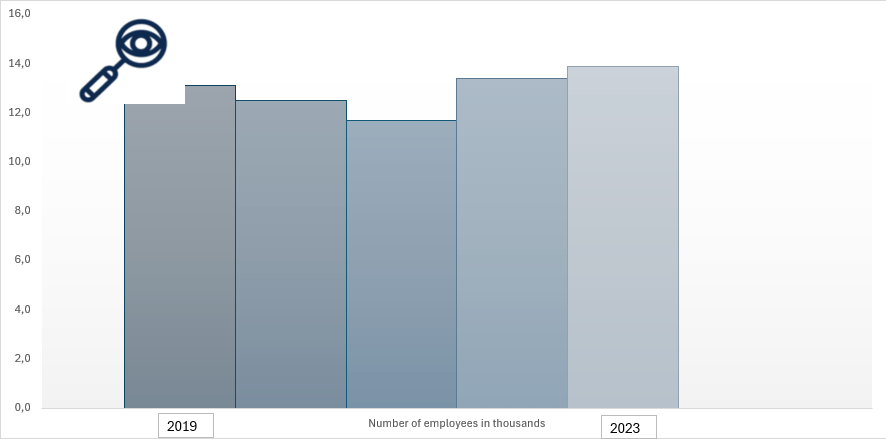

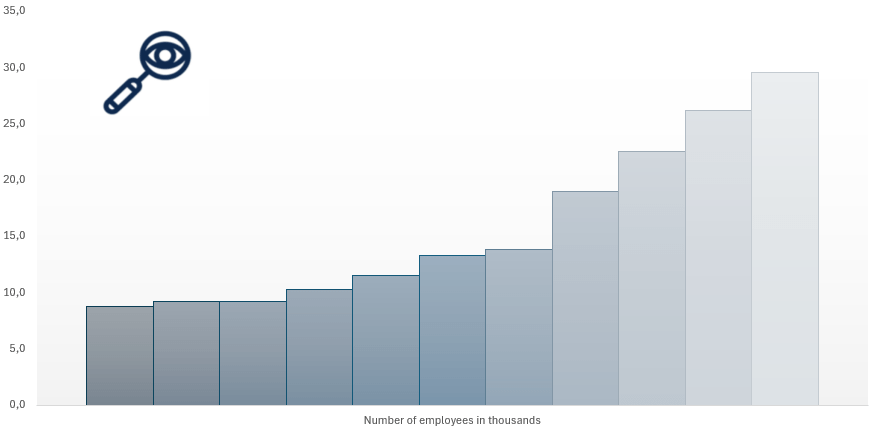

As of the latest data, Canadian Solar employs approximately 22,200 people, reflecting steady growth from around 8,700 employees in 2014. The company was founded in 2001 and is headquartered in Ontario, Canada. It is listed on the NASDAQ exchange under the ticker CSIQ and operates within the Solar Energy industry under the broader Renewable Energy sector. Canadian Solar currently has approximately 73.3 million shares outstanding and a market capitalization of around USD 4.58 billion.

The company’s corporate headquarters is located at 545 Speedvale Avenue West, Guelph, Ontario N1K 1E6, Canada. For more information, you can visit their official website at www.canadiansolar.com.

Illustration 16-18: Number of employees at Canadian Solar and its location in Ontario, Canada.

Canadian Solar presents a promising long-term opportunity, particularly for investors interested in the renewable energy sector. The company is making significant strides in solar energy, energy storage, and utility-scale projects, positioning itself well for the growing demand for sustainable energy solutions. However, its financial health warrants careful consideration.

Although Canadian Solar has a solid asset base, its rising debt levels and increasing liabilities each year contribute to heightened financial risk. A significant portion of its revenue is consumed by costs of goods sold and operating expenses, limiting its profitability. As a result, while Canadian Solar has shown growth, its profitability has been inconsistent, and some of its expansion plans have not met expectations.

From a value investing standpoint, Canadian Solar does not appear to be undervalued, which may make it less appealing for investors seeking stocks with strong financials available at a discount. While the company holds substantial growth potential in the renewable energy sector, it’s crucial for investors to consider the associated risks, especially given its financial structure and profitability challenges. A key concern is that despite the increase in revenue, Canadian Solar’s net profit has remained stagnant, signaling potential inefficiencies or other underlying issues that may affect future profitability. Given these factors, our recommendation is to proceed with caution. If you find our analysis valuable, consider subscribing by entering your email below.

The decision between starting your own business or investing in stocks is one of the most critical financial choices an individual can make. Both paths offer unique opportunities for wealth creation, but they also come with distinct risks and challenges. This article aims to explore all the possible factors to consider when choosing between entrepreneurship and stock market investing, including risk tolerance, capital availability, time commitment, skillset, personal goals, and economic conditions.

Understanding the Fundamentals

Before diving into the key factors, let’s define each option clearly:

Starting a Business involves creating and managing your own company, that offers goods or services. It requires a business idea, operational planning, marketing, and a long-term commitment to growth and management.

Investing in Self-Picked Stocks means selecting and purchasing shares of companies based on research and analysis, aiming for capital appreciation, dividends, or both. This can be everything from small penny stocks to the stocks of some of the biggest and most well established companies in the world.

Investing in stocks and starting a business both involve risk, research, and the potential for long-term wealth, but they differ in control and involvement. Investors rely on companies to grow their money, often passively, while entrepreneurs actively build and manage their businesses.

Both require patience, strategy, and the ability to handle uncertainty, but a business offers more control over success, whereas stocks provide diversification and liquidity. Ultimately, one is about owning a piece of someone else’s success, while the other is about creating your own. Each approach can lead to financial success but in very different ways. The choice depends on individual circumstances, risk appetite, and long-term objectives

1. Risk Tolerance

Starting a Business: Involves high risk, with a significant percentage of startups failing within the first few years. Risks include financial loss, market competition, operational challenges, and economic downturns.

Illustration 1: If entrepreneurship or the stock market is the best alternative depends on how much risk you are willing to take on.

The failure rate if newly started and established companies is quite high. After the first year, about 20% of new businesses fail. After 3 years: Around 45% of businesses fail (~55% survive). After 5 years: Roughly 50%–60% of businesses fail (~40%–50% survive). And after 10 years: Around 70%–90% of businesses fail.

It’s important to note that these figures only reflect business survival rates, not actual success. Among the companies that avoid bankruptcy, 80–90% remain small, with modest profits or just breaking even. Around 5–10% achieve moderate success, growing into stable mid-sized businesses, while 1–5% experience significant growth, becoming highly profitable and expanding nationally or internationally. Fewer than 0.1% reach unicorn status, with a valuation of $1 billion or more. Moderate is here defined as a company that has a net profit of USD 500 000 to USD 20 000 000.

Investing in Stocks: Stock market investments also carry risks, such as market volatility, economic downturns, and company-specific risks. However, diversified investing can help mitigate these risks.

The average person in stock investing tends to underperform the market, with individual investors typically achieving returns around 3%–5% annually, while the S&P 500 historically averages 7%–10% per year, adjusted for inflation. Many investors struggle with poor timing, often buying high and selling low, or making emotional decisions during market volatility. Active traders, trying to pick stocks or time the market, often face higher fees and taxes, which further erode returns. In contrast, those who invest passively in diversified index funds generally align more closely with the market’s long-term average returns, making it a more reliable strategy for most investors.

However, the average stock investor do get a much better return on money, on average, compared to an entrepreneur.

Illustration 2: If you are good with Uncertainty, entrepreneurship can be for you.

Key Consideration: If you have a high-risk tolerance and are comfortable with uncertainty, entrepreneurship could be a good fit. However, if you prefer more calculated risks with the option for diversification, investing in stocks might be the better route. Both options involve risk, but the right choice depends on your personal risk tolerance. Remember, the higher the risk, the greater the potential return—whether you’re choosing stocks or deciding whether to start a business.

2. Capital Requirements

Starting a Business: Starting a business requires significant upfront investment for product development, inventory, marketing, and operational costs. These initial expenses can be substantial, as you’ll need to cover everything from creating your product or service to securing a physical location or paying for website hosting. Rent, employee salaries, and advertising campaigns can also add up quickly. Many entrepreneurs underestimate the financial strain at the beginning, and without enough funding, businesses can easily fail.

You’ll need to save up enough money to cover all these costs before you even start generating income. Inventory purchases, production costs, and operational overheads are not cheap, and it’s easy to feel overwhelmed by the scale of these expenses. If you don’t have the right resources or backup funding, it can be difficult to maintain momentum during the early stages, especially if cash flow is slow. Unlike investing in stocks, which can be done with a relatively small initial capital, starting a business demands a much higher upfront commitment.

Illustration 3: Starting a Business often requires saved capital.

Investing in Stocks: Requires less capital initially. With as little as a few hundred dollars, you can start investing in stocks. While the capital required to start investing in stocks is relatively low, it’s important to remember that achieving significant returns often requires a long-term commitment and a consistent investment strategy. While you can start small, many investors opt to increase their capital gradually, taking advantage of compounding returns. However, it’s essential to be mindful of the costs involved, such as trading fees, commissions, or taxes on dividends and capital gains, which can eat into your profits.

Key Consideration: If you have substantial capital and access to funding, starting a business may be feasible. If capital is limited, stock investing offers a lower barrier to entry.

3. Time Commitment

Starting a Business: Starting a business requires full-time dedication, particularly in the early stages when the foundation is being built. Running a business demands long hours, as entrepreneurs must juggle various tasks, from product development and marketing to managing finances and customer service. It’s a constant cycle of problem-solving and adapting to unforeseen challenges, whether it’s adjusting to market changes, troubleshooting operational issues, or making tough decisions. The ability to remain flexible and resilient is crucial, as the business landscape can shift quickly and often requires entrepreneurs to pivot or refine their approach to stay competitive.

On average, entrepreneurs tend to work 8 to 12 hours a day. In the early stages of a business, this can often stretch beyond 12 hours a day, especially when the entrepreneur is handling multiple roles like marketing, customer service, and operations. As the business matures and more employees are hired, the hours may become more manageable, but many entrepreneurs still put in long days, sometimes working evenings or weekends to stay on top of tasks and ensure the business continues to grow.

Illustration 4: Starting a Business can take significant time.

Investing in Stocks: While active trading requires significant research, long-term investing can be more passive. Stock investing generally requires fewer hours per day compared to running a business. For most investors, he daily time commitment can be quite minimal. On average, investors may spend 30 minutes to an hour a day checking their portfolios, staying updated on market trends, or reviewing the performance of specific stocks.

For those actively trading or managing their investments, it could require more time, possibly 2 to 4 hours a day, particularly if they are making frequent trades or conducting in-depth research. However, stock investing doesn’t typically demand the constant attention that a business requires, and the time commitment can be adjusted based on the investor’s approach—whether it’s passive, active, or a mix of both. If you are picking your own stock, conducting fundamental analysis of all the different companies could take significant time.

Key Consideration: If you prefer flexibility and passive income, stock investing may be a better choice. If you are passionate about building something and willing to dedicate years to it, entrepreneurship might be the way to go.

4. Skillset and Expertise

Starting a Business: Starting a business requires a broad set of skills, including knowledge of business operations, finance, marketing, management, and industry-specific expertise. Entrepreneurs need to understand how to efficiently manage resources, create a profitable business model, and navigate regulatory requirements. Financial knowledge is crucial for managing cash flow, budgeting, and ensuring the business remains solvent. Additionally, marketing and management skills are essential for attracting customers and leading a team, while industry-specific knowledge helps ensure the business can compete effectively in its sector.

Investing in Stocks: Investing in stocks requires a solid understanding of financial markets, stock valuation, economic trends, and risk management. Investors need to assess a company’s financial health, understand how market forces can affect stock prices, and evaluate the potential for future growth. They must also manage risk, which involves diversifying investments and understanding how broader economic conditions can impact their portfolio. Staying informed about global and local market trends, as well as financial reports, is key to making informed investment decisions.

Illustration 5: Expertise is an important factor to take into account.

Key Consideration: f you have strong business acumen and leadership skills, running a business might be a better fit for you. Entrepreneurship allows you to directly apply your skills in management, problem-solving, and decision-making. On the other hand, if you enjoy analyzing companies, financial data, and understanding market trends, stock investing could be a better option. Both paths require a keen understanding of numbers, but the level of involvement and the type of expertise needed differ significantly.

5. Potential Returns and Scalability

Starting a Business: Starting a business can offer unlimited earnings if successful, but profits depend heavily on execution, market demand, and the scalability of the business model.